This guide explains the basics, why scores differ, and a simple plan to improve without overthinking it.

1

Key takeaways

- You don’t have just one score—scores vary by bureau and scoring model/version. 2

- Across most models, the biggest wins are: pay on time and keep credit-card balances low. 3

- Check your credit reports regularly and fix errors early (especially before applying for credit or renting). 5

1) What a credit score is

A credit score is a number that predicts how likely you are to repay debt on time, based on information in your credit reports.

Lenders use it to decide approvals, credit limits, and interest rates.

1

Different lenders may use different scores and versions.

2

2) Credit score vs credit report

The most common confusion is mixing these up:

| Credit report | Credit score |

|---|---|

| Detailed file: accounts, balances, payment history, inquiries, and other reported data. | A number produced when a scoring model analyzes report data. |

| Can differ by bureau because not every lender reports to all bureaus. | Can differ by model (FICO vs VantageScore), version, and lender use-case. |

A simple analogy: credit report = transcript, credit score = GPA.

2

3) Why you don’t have “one” credit score

It’s normal to see different numbers because:

- Different bureaus can have slightly different data (reporting isn’t identical everywhere).

- Different scoring models exist (and multiple versions of each model).

- Different lender needs (some use industry-specific scores or internal scorecards).

Don’t chase a single number—focus on the habits that help across most models: pay on time and keep revolving balances low.

2

4) What affects a credit score (the factors that matter)

Scoring models vary, but FICO commonly groups scoring into five categories (with typical weightings).

3

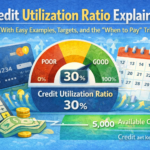

Utilization (the “reported balance ÷ limit” idea)

Utilization is essentially your reported balance divided by your credit limit. Even if you pay in full, the balance that gets

reported (often the statement balance) can affect your score.

4

4

5) What’s a “good” credit score?

Many commonly used scores fall in a 300–850 range, but not all scoring models use the same scale.

Lenders also set their own approval tiers.

1

Instead of obsessing over a label (“good/excellent”), aim for habits that improve approvals and pricing: on-time payments, low balances,

and fewer unnecessary applications.

2

6) A simple plan to improve your credit score

Step 1: Protect payment history

Set autopay for the minimum on every account to prevent accidental late payments. Then pay extra manually when you can.

3

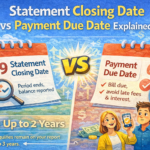

Step 2: Lower utilization (smart + fast)

- Pay down balances before the statement closes (so a lower balance gets reported).

- Avoid running cards near the limit (even temporarily) if you’re about to apply for something.

CFPB guidance emphasizes that high reported balances can affect scores even if you pay soon after.

4

Step 3: Apply less, win more

Multiple applications in a short window can lower your score temporarily. Apply with a plan—especially before a big goal (apartment, auto loan, mortgage).

2

Step 4: If you’re “thin file,” build safely

Common starter paths include secured cards, becoming an authorized user (with someone who pays on time and keeps low balances),

or credit-builder products offered by some credit unions (availability varies). The goal is clean payment history—not bigger debt.

7) Free credit reports (and fixing errors)

How to check your credit reports for free

In the U.S., you can request free credit reports through the official channel: AnnualCreditReport.com.

CFPB guidance also notes you can access reports more frequently online (including weekly access).

5

How to fix errors

If something looks wrong, dispute it with the credit reporting company and (when appropriate) the company that furnished the information.

CFPB and FTC consumer guidance walk through the process and documentation basics.

6 7

8) Why credit scores can cost real money (simple example)

Example math (illustrative): a $15,000 auto loan for 60 months:

14% APR → payment ≈ $349.18/mo → total interest ≈ $5,950.53

Difference in interest ≈ $3,552.31 (same loan amount, different rate)

Rates and approvals depend on the lender, market, and your full application—not just one score. Use the example to understand scale, not to predict an offer.

FAQ

Does checking my own credit hurt my score?

Checking your own report/score is generally different from applying for credit. Applications can involve “hard inquiries,” which may affect scores.

(If unsure, ask the lender what type of inquiry they use.)

2

Do I need to carry a credit-card balance to build credit?

You don’t need to pay interest to build credit. What matters is on-time payments and the balances that get reported.

Paying in full is fine—just watch utilization if your reported balance is high.

4

Why did my score drop even though I paid on time?

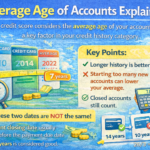

Common reasons: a higher reported card balance, a new inquiry, a new account lowering average age, or an error in the report.

6

References

-

Consumer Financial Protection Bureau (CFPB). “What is a credit score?” (Ask CFPB)Definition, common score range, and why lenders use scores.

-

CFPB. “Why are there differences between credit scores?” (Ask CFPB) + “Understanding Differences in Credit Scores” reportWhy you may see different scores across bureaus and scoring models/versions.

-

myFICO (FICO). “What’s in my FICO Scores?” (credit scoring factors and typical weightings)FICO category breakdown (payment history, amounts owed, length of history, new credit, mix).

-

CFPB. “Will paying off my credit card balance every month improve my credit?” (Ask CFPB)Reported balances/utilization and why timing can matter.

-

CFPB. Free credit reports (AnnualCreditReport.com) guidanceHow to request your credit reports through the official channel; frequency/availability can change over time.

-

CFPB. Disputing credit report errors (consumer guidance)How to dispute errors and what documentation helps.

-

Federal Trade Commission (FTC). Disputing errors on credit reportsPractical dispute steps and records to keep.

Disclosure: This article is general education, not financial advice. Credit scoring, lender criteria, and reporting practices vary by bureau, lender, product, and time.