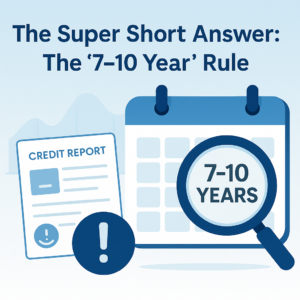

Quick answers

- Most negativesUp to 7 years under the FCRA (timing depends on item and start date).1

- Charge-offs / collectionsOften described as 7 years + 180 days, anchored to the delinquency that led to the negative item.1

- BankruptcyCan be reported for up to 10 years (maximum reporting period).1

- Good newsScore impact usually fades before the item disappears if newer behavior is clean (on-time payments + low utilization).

For many major negatives, the reporting window is anchored to the first missed payment that started the chain (if you never brought the account current again).1

Credit report timeline table (common items)

These are typical FCRA maximum reporting windows. Your credit report often shows an “estimated removal” month for each item.

| Negative item | Typical maximum time it can appear | What usually starts the clock |

|---|---|---|

| Late payment (30/60/90+) | Up to ~7 years1 | The month it first became late |

| Collection account | Often up to ~7 years (commonly described as tied to DOFD)1 | The delinquency that led to collection (not “when it was sold”) |

| Charge-off | Often described as ~7 years + 180 days1 | The delinquency that led to the charge-off |

| Foreclosure / repossession | Often up to ~7 years1 | Usually follows the delinquency timeline |

| Hard inquiry | Up to 2 years on the report1 | Date of inquiry |

| Bankruptcy | Up to 10 years (maximum)1 | Filing/court timeline |

Date of First Delinquency (DOFD): why “7 years” confuses people

If a debt went delinquent and was never brought current again, the FCRA’s reporting window for certain major negatives is

anchored to that delinquency chain (this is why a collection can show an “opened” date that looks newer than the start of the 7-year window).1

Does paying reset the clock?

Generally, no. The reporting timeline is anchored to the delinquency event that led to the negative item—not the last payment or the last time a collector contacted you.

(Paying can still matter for approvals, lender decisions, and peace of mind—just don’t expect it to restart the FCRA timer.)1

How long it “hurts” vs how long it “shows”

A big beginner trap is assuming visibility = maximum impact. Many scoring models weigh recent problems more heavily than old ones.

If you stop new late payments, keep revolving balances low, and build clean months, your score can improve while the old item still appears.

Credit reporting time limit vs statute of limitations

These are different rules:

- Credit reporting (FCRA)How long an item can appear on your credit report.1

- Statute of limitations (state law)How long a creditor might have to sue to collect (varies by state and debt type).

Medical debt (what’s reliable to say in 2026)

Medical debt reporting has changed in recent years and can also be affected by state laws. One widely reported change:

the major bureaus agreed to stop reporting certain small medical collections (for example, amounts under $500).5

Practical move: don’t rely on headlines—pull your reports and see what’s actually listed.

How to check if something should have fallen off already

-

1Pull your reports from the official free source (AnnualCreditReport.com).2

-

2Look for the delinquency timeline fields and the bureau’s “estimated removal” date (wording varies by bureau).

-

3If the item appears older than allowed, dispute it as obsolete (beyond the reporting period). FTC guidance explains dispute basics and next steps.3

What to do now (better than waiting 7 years)

-

1Turn on autopay for minimums everywhere (then pay extra manually). This prevents accidental late payments.

-

2Lower revolving utilization (fastest common score lever month-to-month).

-

3Avoid unnecessary hard inquiries while you’re rebuilding.

-

4Check reports periodically and dispute errors (especially duplicates, wrong balances, or wrong delinquency dates).3

FAQ

Does paying a collection reset the 7-year clock?

Usually no—the reporting timeline is generally tied to the delinquency that led to the collection/charge-off chain.1

Can accurate negatives be removed early?

Typically they remain until they age off, unless you’re disputing errors or obsolete items beyond the reporting period.

How often should I check my reports?

If you’re rebuilding, checking periodically (and before major applications) is reasonable. Free reports are available via the official source.2

References

Click a number in the article to jump here. Click “Source” to open the original site.

15 U.S.C. § 1681c — FCRA “Obsolete information” reporting limits (Cornell Law School)

Primary source for maximum reporting periods (7 years; 7 years + 180 days for certain items; 10-year bankruptcy; 2-year inquiries).

FTC — Free credit reports (AnnualCreditReport.com)

Official guidance on getting free credit reports and how often you can access them.

FTC — Disputing errors on credit reports

How to dispute incorrect or outdated information and what to expect from the dispute process.

AP News — Medical debt reporting context (bureaus’ under-$500 change referenced)

Reporting that discusses medical debt credit-report changes, including the bureaus’ agreement to stop reporting certain small medical collections.

Research-focused writing built from primary consumer/regulator sources and updated when guidance changes.

•

Disclosure: General education, not legal advice.