Written by MrHamza, Credit Score Educator for Beginners

How Credit Scores Are Calculated? If you’ve ever checked your credit score and thought:

“Why did it just drop 15 points when I didn’t do anything crazy?”

…this article is for you.

The truth is:

- There is no single universal formula that everyone uses.

- Different companies (like FICO and VantageScore) have their own scoring models.

- But they mostly look at the same core ingredients in your credit reports with slightly different recipes. Consumer Financial Protection Bureau+1

In this guide, we’ll walk through:

- The actual factors that go into most credit scores

- Rough percentages used by popular models like FICO

- A simple, real-life “what-if” example so you can see how behavior changes your score over time

All in plain English, for beginners.

1. Big Picture: How Credit Scores Are Built

Credit scores don’t come from your bank account balance or your salary.

They are calculated from data in your credit reports, which come from the three major credit bureaus:

- Equifax

- Experian

- TransUnion

Scoring companies (like FICO and VantageScore) pull the info in those reports and apply their own formulas.

According to FICO, their scores are based on five broad categories of information: myFICO+2MyCreditUnion.gov+2

- Payment history

- Amounts owed (credit utilization & debt)

- Length of credit history

- New credit

- Credit mix

The Consumer Financial Protection Bureau (CFPB) lists almost the same ideas in its explanation of what affects your score: your bill-paying history, unpaid debt, how long accounts have been open, the types of loans you have, your use of available credit, and new applications. Consumer Financial Protection Bureau

Key idea:

Each model uses its own secret math, but the same 5–6 big factors show up again and again.

2. The FICO “Recipe”: 5 Factors and Their Approximate Weights

FICO doesn’t reveal the full formula, but it does share how important each category usually is in its standard 300–850 score: Zilch | US+3myFICO+3Investopedia+3

| FICO Factor | Approx. Weight |

|---|---|

| Payment history | 35% |

| Amounts owed (utilization) | 30% |

| Length of credit history | 15% |

| New credit | 10% |

| Credit mix | 10% |

Think of your score like a pizza. Some slices (like payment history) are much bigger than others (like credit mix).

Below, we’ll break each factor down with examples and beginner-friendly tips.

3. Payment History (≈35%) – The “Did You Pay On Time?” Slice

This is the single most important part of most credit scores.

It looks at:

- Have you paid past accounts on time?

- How often have you been late?

- How late (30, 60, 90+ days)?

- Do you have any collections, charge-offs, or bankruptcies?

According to FICO and multiple educational sources, payment history is roughly 35% of your FICO score. myFICO+2MyCreditUnion.gov+2

Why so heavy?

Because the best predictor of whether you’ll pay future bills is how you’ve handled past ones.

Recent data backs this up: as delinquencies (late payments 90+ days past due) increased in 2025, average credit scores started to tick down across all score tiers — even among “superprime” borrowers. Investopedia+1

Real-World Example: One Late Payment

Imagine:

- You’ve had a credit card for 3 years

- Always paid on time

- Your score is around 720 (solid “Good” range)

Then you have one bad month:

- You miss a payment by 35 days

- The lender reports it as 30-days late

Result?

- Your score could drop dozens of points (exact number depends on your profile)

- That late mark can stay on your report for several years, even after you catch up

Beginner rule: Above everything else, protect your on-time payment history. Autopay and reminders are your best friends.

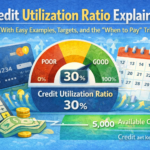

4. Amounts Owed & Credit Utilization (≈30%) – How Much of Your Credit You Use

This factor looks at how much debt you’re carrying, especially on revolving credit like credit cards.

A huge piece of this is credit utilization:

Credit utilization = how much of your available credit you’re using.

Example:

- You have a card with a $2,000 limit

- Your current balance is $1,600

- Utilization = 1,600 / 2,000 = 80% (very high)

Beginners often don’t realize that high utilization can hurt your score even if you never miss a payment.

Most experts and educational sites suggest: Experian+2TransUnion+2

- Try to stay under 30% utilization overall

- Under 10% is even better if you’re chasing top-tier scores

Real-World Example: Paying Down a Card

Let’s say:

- Total credit limit across all cards: $3,000

- Current balances: $2,400

- Utilization = 2,400 / 3,000 = 80%

That’s a big red flag to scoring models.

You decide to attack the balance:

- You pay it down to $900

- New utilization = 900 / 3,000 = 30%

What typically happens:

- You’ve just improved a 30%-weight factor in your FICO score recipe

- It’s common to see noticeable score increases over the next month or two as your lower balances get reported (exact points vary)

Beginner move: If your cards are near maxed out, focus on paying them down even a bit. Getting utilization down from “maxed” to “reasonable” often gives you faster score improvement than anything else besides fixing late payments.

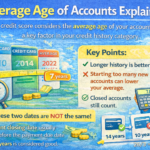

5. Length of Credit History (≈15%) – How Long You’ve Been in the Game

This factor checks:

- How long your oldest account has been open

- The average age of all your accounts

- How long it’s been since you used certain accounts

FICO says this category makes up about 15% of your score. myFICO+2Investopedia+2

Why it matters:

- Lenders feel more comfortable when they can see a long track record of responsible credit use.

- Newer files = less data = more uncertainty.

Example: Average Age of Accounts

Imagine two beginners:

Person A:

- 1 credit card opened 4 years ago

- 1 student loan opened 3 years ago

Average age: (4 + 3) / 2 = 3.5 years

Person B:

- 1 credit card opened 6 months ago

- 1 store card opened 2 months ago

Average age: (0.5 + 0.17) / 2 ≈ 0.33 years

Even if they both pay on time, Person A may have an advantage purely because their accounts have been around longer.

Beginner move: Don’t open and close accounts constantly. Let good, low-stress accounts age.

6. New Credit (≈10%) – How Often You’re Applying

This factor looks at:

- How many new accounts you’ve opened recently

- How many hard inquiries (lenders pulling your report for a real application) have hit your file

FICO lists this category at about 10% of the score. myFICO+2MyCreditUnion.gov+2

A handful of hard inquiries over a year or two is normal.

But many applications in a short time can make you look like you’re scrambling for credit.

Good to know:

- Hard inquiries (real applications for credit) can cause a small, temporary dip.

- Soft inquiries (you checking your own score, pre-qualification checks) do not affect your score. Consumer Financial Protection Bureau+1

Example: Two Different Approaches

- Person A applies for 1 new card this year → 1 hard inquiry, no big deal.

- Person B applies for 6 cards in 2 months → multiple hard inquiries + new accounts = score likely drops more noticeably.

7. Credit Mix (≈10%) – Types of Credit You Use

This factor cares about variety:

- Revolving credit – credit cards, store cards

- Installment loans – auto loans, student loans, mortgages, personal loans

FICO generally puts this at about 10% of your score. myFICO+2MyCreditUnion.gov+2

You don’t need every single type of account.

But having only one small store card and nothing else is a thinner profile than someone with:

- A major credit card

- A student or auto loan

- A history of paying both well

Important: Never take on a loan you don’t need just to improve “credit mix.” It’s the smallest slice of the pie.

8. VantageScore’s Take: Similar Ingredients, Different Recipe

While FICO is used by many lenders, VantageScore is another major scoring model used across the US.

VantageScore 3.0 and 4.0 use slightly different categories and weights, but again, the same ideas show up. Educational material from VantageScore gives a breakdown like: Jenius Bank+4VantageScore+4equifax.com+4

Example (VantageScore 4.0, approximate):

- Payment history – around 41%

- Depth/age of credit – around 20%

- Credit utilization – around 20%

- Recent credit – around 11%

- Balances – around 6%

- Available credit – around 2%

What you should notice:

- Payment history is still the biggest factor.

- How much you owe / use is still very important.

- The smaller stuff is still about time, variety, and new accounts.

So even though FICO and VantageScore are different companies:

If you treat your credit well, both scores usually move in the same direction.

9. What’s Not in the Formula (But People Think It Is)

Many beginners assume certain things affect their score that actually don’t.

According to the CFPB and other official sources, credit scores do not directly include: Consumer Financial Protection Bureau+2LendingClub+2

- Your income

- Your job title or employer

- Your marital status

- Your race, gender, or religion

- Your debit card usage

- Your savings account balance

Those things can matter to lenders in other ways (for example, they might ask about your income separately when you apply), but they are not part of your credit report data used for most scores.

10. Step-by-Step: How Your Monthly Behavior Turns Into a Score

Let’s make this super concrete.

Imagine Maria, a beginner in the US:

- 1 credit card, $1,500 limit

- 1 small auto loan

- She’s been using credit for 2 years

- Her score is around 690 (upper “Fair” / lower “Good”)

Month 1 – High Utilization

- Her card is almost maxed: $1,350 / $1,500 → 90% utilization

- She pays on time, but only the minimum

- When the card reports that $1,350 balance, her score drops a bit because the 30%-weight “amounts owed” factor looks worse.

Month 2 – Pays Down the Card

- She gets a small tax refund and side gig money

- Pays the card down to $450

- New utilization = 450 / 1,500 → 30%

When this lower balance gets reported:

- The “amounts owed” slice improves

- Her score moves up, maybe bouncing above 700, even though her income and job didn’t change

Month 3 – One Late Payment

- She forgets her auto loan payment

- It’s reported as 30-days late

Result:

- The 35%-weight “payment history” slice takes a hit

- Her score drops more sharply than when her utilization changed

- She sets up autopay so it doesn’t happen again

Over the next 6–12 months:

- On-time payments + lower utilization slowly pull her score back up

- That late mark hurts less as it gets older, especially if she doesn’t add new problems

Same person. Same job. Same city.

Different behavior → different score. That’s how the calculation works in real life.

11. Quick FAQ: Calculation & Key Factors

Q1: Is my score literally “35% payment history + 30% utilization” like a school grade?

Not exactly. Those percentages are guidelines, not exact formulas. FICO itself says your exact score depends on the whole picture in your credit report, but those ranges show what tends to matter most. myFICO+2Better Money Habits+2

Q2: Can one late payment really cause a big drop?

Yes. Especially if you previously had a very clean history. Some VantageScore educational sources note that a single late payment can cause a drop of well over 100 points in extreme cases — the exact number depends on your starting profile. Jenius Bank+1

Q3: Does checking my own score hurt the calculation?

No. Checking your own score (through a bank, app, or credit monitoring site) is a soft inquiry and doesn’t affect your score. Only hard inquiries from real applications for credit can cause small, temporary dips. Consumer Financial Protection Bureau+1

Q4: Are all credit scores FICO?

No. FICO is very widely used, but many lenders and apps also use versions of VantageScore or other models. They all use similar factors but may weigh them differently.

Q5: Why do I see different scores from different places on the same day?

Because:

- They might be using different models (FICO vs VantageScore)

- They might be looking at different bureaus (Experian vs TransUnion)

- They might be using older vs newer versions of the same model

That’s normal. You’re looking for your general range and direction, not a single “perfect” number.

12. Turning This Knowledge into Action

Now that you know how scores are calculated, here’s how to use it:

- Protect payment history (35–40%):

- Autopay + reminders

- Call creditors early if you’ll struggle to pay

- Tackle utilization (20–30%):

- Avoid maxing cards out

- Pay them down whenever you can

- If possible, pay before the statement date so lower balances get reported

- Let accounts age (15–20%):

- Don’t keep opening new cards for random reasons

- Think long-term with your main accounts

- Be picky about new credit (5–10%):

- Only apply when you have a purpose

- Don’t shotgun applications everywhere in one weekend

- Don’t stress too much about “credit mix” (≈10%):

- Having both a card and an installment loan can help

- But never borrow just to get “a mix”

Mrhamza:

Money basics writer • Credit scores, reports, and everyday finance explainers

Research-focused writing built from primary consumer/regulator sources and updated when guidance changes.

About the author

Editorial policy

Corrections •

Disclosure: General education, not legal advice.