Written by MrHamza, Credit Score Educator for Beginners

credit utilization ratio Explained : If you’ve ever checked your credit and seen something like:

“You’re using 76% of your available credit.”

…you might have thought:

“Okay, but is that good? Bad? And what am I supposed to do about it?”

That “76%” is your credit utilization ratio (or credit usage) — and it’s one of the most powerful levers you control when it comes to your credit score.

In fact:

- FICO says “amounts owed” (which includes how much of your credit limits you’re using) makes up about 30% of a typical FICO score. myFICO

- TransUnion estimates “credit usage” at 34% of its score breakdown, with credit utilization alone around 20% of that. TransUnion

- The CFPB (Consumer Financial Protection Bureau) and other experts suggest keeping your use of credit below 30% of your total limits — and lower is better. Consumer Financial Protection Bureau+1

So yeah, this number matters.

In this guide, I’ll explain what credit utilization is, how to calculate it, and show you step-by-step examples so you can see exactly how to improve it.

1. What Is the Credit Utilization Ratio?

Let’s keep it super simple:

Your credit utilization ratio is the percentage of your available revolving credit that you’re using.

- It mostly applies to credit cards and lines of credit (revolving accounts). Capital One+2equifax.com+2

- It does not usually include installment loans (like auto loans or student loans) in the actual “utilization” formula, although those still matter for your overall debt picture.

Official explanations say basically the same thing:

- Capital One: credit utilization measures how much credit you’ve used versus how much you have, as a percentage. Capital One

- Equifax: it’s the amount of revolving credit you’re using divided by the total available revolving credit. equifax.com

- TransUnion: it’s how much credit you’re using compared to your total credit limit. TransUnion

- Experian: your utilization rate is the percentage of available credit you’re using; lower is generally better. Experian

Key idea:

The higher your utilization, the more it looks like you’re leaning heavily on credit — which makes scoring models nervous.

2. How to Calculate Your Credit Utilization (Step-by-Step)

The formula is the same everywhere:

Credit utilization (%) = (total revolving balances ÷ total revolving limits) × 100

The CFPB and multiple banks give the exact same steps: add up your balances, add up your limits, then divide and multiply by 100. Consumer Financial Protection Bureau+1

Example 1: One Credit Card

Let’s say you have:

- Credit card limit: $1,000

- Current balance: $600

Calculation:

- Utilization = $600 ÷ $1,000 = 0.60

- As a percentage: 0.60 × 100 = 60%

So your credit utilization is 60%.

Experts (like the CFPB) say that’s too high — they recommend keeping it at 30% or less, and many credit educators suggest under 10% if you’re really trying to optimize your score. Consumer Financial Protection Bureau+1

Example 2: Multiple Cards – Total Utilization

Now let’s say you have three cards:

| Card | Limit | Balance |

|---|---|---|

| Card A | $1,000 | $300 |

| Card B | $2,000 | $900 |

| Card C | $500 | $0 |

Step 1 – Add up all limits:

$1,000 + $2,000 + $500 = $3,500 total limit

Step 2 – Add up all balances:

$300 + $900 + $0 = $1,200 total balance

Step 3 – Divide balance by limit:

$1,200 ÷ $3,500 ≈ 0.343

Step 4 – Convert to percentage:

0.343 × 100 ≈ 34.3%

Your overall credit utilization is about 34%.

That’s a bit above the commonly suggested 30% cap, but much better than 60–80% or being maxed out.

Example 3: Per-Card vs Total Utilization

Most scoring models look at both:

- Your overall utilization

- Your utilization on individual cards TransUnion+1

Using the same numbers:

- Card A: $300 / $1,000 = 30%

- Card B: $900 / $2,000 = 45%

- Card C: $0 / $500 = 0%

Total: 34.3%

So even though your overall utilization is okay-ish, Card B at 45% might still make you look a bit “stretched” on that particular card.

Beginner tip:

Aim for both: keep your overall utilization low and avoid maxing any single card.

3. Why Credit Utilization Matters So Much for Your Score

Scoring companies have been very clear:

- FICO says “amounts owed” (including utilization) account for 30% of a FICO score. myFICO

- TransUnion’s scoring breakdown puts “credit usage” (utilization + balances + available credit) at 34% of the score, with utilization itself at about 20%. TransUnion

At the same time, real-world data shows people are using more of their available credit:

- A recent FICO-based report shows US credit utilization rates have climbed from about 29.6% in 2021 to 35.5% in 2025, alongside higher overall credit card debt and rising delinquencies. Investopedia

Why scoring models care:

- If you’re regularly using 70–90% of your limits, it signals you might be at risk of financial strain.

- Even if you’re paying on time, very high utilization looks riskier than someone who uses credit lightly.

Simple translation:

High utilization = “This person leans hard on credit.”

Low utilization = “This person has breathing room.”

4. Simple Before-and-After Utilization Examples

Let’s walk through specific situations you can picture.

Example 4: Paying Down a Maxed-Out Card

You have:

- 1 card

- Limit: $2,000

- Balance: $1,800

Utilization:

- $1,800 ÷ $2,000 = 90% → 🚨 Very high

This is the kind of number that can drag your score down even if you’ve never missed a payment.

You decide to start knocking it down:

Step 1 – Pay down to $1,000

- New balance: $1,000

- Utilization: $1,000 ÷ $2,000 = 50%

Better, but still high.

Step 2 – Pay down to $600

- New balance: $600

- Utilization: $600 ÷ $2,000 = 30%

Now you’ve hit the classic “at or under 30%” zone that many experts recommend. Consumer Financial Protection Bureau+1

Step 3 – Pay down to $200

- New balance: $200

- Utilization: $200 ÷ $2,000 = 10%

Here, you’re in “very low utilization” territory: you use your card, but you’re far from maxed out.

Important: You don’t have to hit 0% for a healthy score.

Many people with strong scores sit in the 1–10% range.

Example 5: Same Debt, Different Distribution

You owe $2,000 total across cards.

Two different ways to arrange it:

Option A – All on One Card

- Card A: limit $2,000, balance $2,000 → 100%

- Card B: limit $1,000, balance $0 → 0%

Total limits: $3,000

Total balance: $2,000

Overall utilization: 2,000 ÷ 3,000 ≈ 67%

Per-card:

- Card A: 100% (maxed out)

- Card B: 0%

Option B – Spread Out

- Card A: limit $2,000, balance $1,000 → 50%

- Card B: limit $1,000, balance $1,000 → 100%

Total limits: $3,000

Total balance: $2,000

Overall utilization: still 67%

Per-card:

- Card A: 50%

- Card B: 100%

Notice:

- Overall utilization is exactly the same (67%) in both cases.

- But having any card at 100% (maxed) looks risky.

Beginner move:

Try to avoid letting any single card sit at or near 100%, even if your total utilization looks okay. Spreading balances can help, but the bigger win is to pay them down.

Example 6: How Closing a Card Can Hurt Utilization

This one surprises a lot of beginners.

Let’s say you have:

| Card | Limit | Balance |

|---|---|---|

| Card A | $2,000 | $500 |

| Card B | $3,000 | $0 |

Total limit = $5,000

Total balance = $500

Utilization = 500 ÷ 5,000 = 10% → Excellent

You think:

“I never use Card B anyway, I’ll just close it.”

After closing Card B:

- New total limit = $2,000

- Balance = $500

New utilization = 500 ÷ 2,000 = 25%

You’ve done nothing wrong with payments — but your utilization has jumped from 10% to 25% just by closing a zero-balance card.

The CFPB warns about exactly this: closing a card can increase your credit utilization ratio and lower your score because you have less available credit. Consumer Financial Protection Bureau+1

Before closing a card, always check what it will do to your total limits and utilization.

5. What’s a “Good” Credit Utilization Ratio?

There’s no universal magic number, but guidance from regulators and major lenders is very consistent:

- The CFPB: try to keep your use of credit at no more than 30% of your total limits. Consumer Financial Protection Bureau

- CFPB myth-busting blog: a lower utilization ratio is better; paying off your entire balance keeps it low and strengthens your scores. Consumer Financial Protection Bureau

- Experian, TransUnion, and others echo the same idea: lower is better, especially under 30%. Experian+2TransUnion+2

Simple rule of thumb for beginners:

- Under 30% = Okay / safe zone

- Under 10% = Great for score-building

- Over 50% = Starting to look risky

- Over 80–90% or maxed = Big red flag

6. Does Credit Utilization Count If I Pay in Full Every Month?

This is a really common confusion.

Even if you pay your card off in full every month, your reported balance might not be $0.

Here’s why:

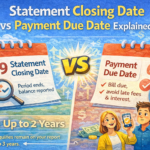

- Most card issuers report your balance to the bureaus around your statement closing date, not your due date.

- If you use your card heavily all month, your statement cuts with a big balance, and then you pay in full, the credit bureaus may still see a high utilization.

Trick:

If you’re prepping for a big application (like a mortgage or a new card), you can pay down your card before the statement closing date so a lower balance is reported.

You don’t need to obsess over daily timing all the time, but it matters in the short term when you’re about to apply for something important.

7. Simple Ways to Improve Your Credit Utilization

Let’s turn this into action. These tips are also echoed by Experian, the CFPB, and other education sources. Experian+2Consumer Financial Protection Bureau+2

1. Pay Down Your Balances

Obvious but powerful:

- Even small extra payments chip away at high utilization.

- Focus first on cards that are maxed out or in the 60–100% range.

If you can only do a little, that’s still progress.

2. Make Multiple Payments During the Month

Instead of:

- Charging all month

- Making one payment after the statement

Try:

- Paying once mid-month and again before the due date.

This keeps your reported balance (and utilization) lower and more stable.

3. Ask for a Credit Limit Increase (Carefully)

If you have a good payment history, some issuers may raise your limit.

Example:

- Old limit: $1,000, balance: $300 → 30%

- New limit: $2,000, same balance: $300 → 15%

Credit utilization is lower without paying extra.

But be careful:

- Don’t ask for increases if you know it will tempt you to spend more.

- Some increases involve a hard inquiry, which can temporarily ding your score a bit.

Experian suggests limit increases as one tool among several to keep utilization low. Experian

4. Spread Out Your Spending (But Don’t Game It Too Hard)

If you have multiple cards:

- Avoid maxing out one card while others sit at 0%

- Spread purchases so no single card is overloaded

This can help both per-card utilization and your overall picture. Just watch that you’re not making it harder to keep track of payments.

5. Keep Old, Fee-Free Cards Open

As we saw in Example 6:

- Closing a card reduces your total limit

- That can increase your utilization even if your balances don’t change

If a card has no annual fee and isn’t a fraud risk, consider:

- Keeping it open

- Using it occasionally for a small purchase

- Setting an autopay to avoid accidental inactivity

The CFPB explicitly notes that closing a card can raise your utilization and lower your score. Consumer Financial Protection Bureau

6. Don’t Take on New Debt Just to “Fix” Utilization

Personal loans and balance transfers can change how your debt is counted, but you’re still in debt.

- A personal loan won’t count toward credit card utilization directly, but it still affects your overall credit picture and budget. LendingClub+1

- The real goal is to reduce what you owe, not just shuffle balances around.

8. Quick FAQ on Credit Utilization

Q1: Do installment loans (like car loans) count in my utilization ratio?

Not usually in the credit utilization formula. That ratio is mainly about revolving accounts like credit cards and lines of credit. Installment loans still matter for your score, but in different ways (total debt, payment history, etc.). LendingClub+1

Q2: Is 0% utilization the best?

Not necessarily. Having some activity (like 1–10%) shows you use credit and manage it well. A completely inactive card may sometimes risk closure. Many high-score profiles sit in the single-digit utilization range.

Q3: Do I need to carry a balance and pay interest to build credit?

No. The CFPB specifically debunks this myth: you don’t need to carry a balance. Paying your balance in full is best and keeps your utilization low, which strengthens your credit. Consumer Financial Protection Bureau

Q4: How fast does changing utilization affect my score?

When your card issuer reports your new, lower balance to the bureaus (often monthly), your utilization changes in your credit file. That means your score can improve relatively quickly compared with long-term factors like account age.

Q5: What’s happening in the real world with utilization right now?

Recent reports show US credit card utilization has risen to around 35.5%, up from about 29.6% a few years earlier — a sign that more people are leaning on credit amid higher prices and interest rates. Investopedia

9. Final Thoughts: Utilization Is One Lever You Really Control

Some parts of your score are slow to change (like how long you’ve had credit).

But credit utilization is something you can start improving this month, even with small steps.

If you remember just three things from this article, let them be:

Paying down balances + not closing good old cards = powerful combo.

Credit utilization = balances ÷ limits.

Lower is better — aim for under 30%, and under 10% if you can.

Mrhamza:

Money basics writer • Credit scores, reports, and everyday finance explainers

Research-focused writing built from primary consumer/regulator sources and updated when guidance changes.

About the author

Editorial policy

Corrections •

Disclosure: General education, not legal advice.