- Credit limit = the maximum your issuer lets you borrow on that card.

- Balance = what you currently owe right now.

- Available credit = limit − balance.

- The score-relevant part is usually the ratio: utilization = balance ÷ limit.

1) What is a credit limit?

Your credit limit is the maximum amount your card issuer allows you to spend/borrow on that credit card.

Think of it as the ceiling for that account.12

What your limit is based on

- Your credit history and risk profile

- Your income and existing debts

- How you’ve managed accounts with that issuer

2) What is a credit card balance?

Your credit card balance is the amount you owe on the card.

It changes as you make purchases, fees/interest post, and you make payments.

Many apps show multiple “balances” — here’s what they usually mean.1

| Term | What it means | Why you should care |

|---|---|---|

| Current balance | What you owe right now (includes purchases after your last statement closed). | Helps you avoid overspending and track what you actually owe today. |

| Statement balance | The balance on the day your billing cycle ended (your statement “snapshot”). | Paying this in full by the due date is the common way to avoid purchase interest (when you have a grace period). |

| Minimum payment | The smallest amount required to keep the account current. | Paying only the minimum can keep you in debt a long time and cost more in interest. |

| Available credit | Your remaining room to spend: limit − current balance. | This is what “feels” like you can still spend — but spending more raises utilization. |

3) Credit limit vs balance (simple table)

| Term | What it means | Who controls it most? | How often it changes |

|---|---|---|---|

| Credit limit | Maximum allowed borrowing on the card | Issuer (you can request changes) | Occasionally |

| Balance | What you currently owe | You (spend + payments) | Frequently |

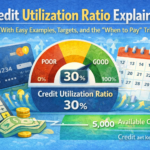

4) Why the difference matters for your score: credit utilization

The part that impacts scores the most is typically utilization — how much of your available credit you’re using.

A common guideline is to keep utilization below about 30%, and lower is generally better.4

Example (one card)

- Limit: $3,000

- Balance: $1,500

- Utilization: $1,500 ÷ $3,000 = 0.50 = 50%

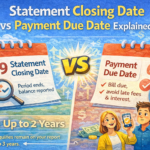

Credit scores use the balance information lenders report to the credit bureaus (often monthly).

Even if you pay in full by the due date, a high statement-closing balance can still temporarily show up as high utilization.

Paying earlier (before the statement closes) can reduce the balance that gets reported.3

5) Real-life examples (so it really clicks)

Example A: Same balance, different limits

- Person 1: $600 balance on a $1,000 limit → 60% utilization

- Person 2: $600 balance on a $3,000 limit → 20% utilization

Same $600 debt, but one looks much closer to “maxed out” because the limit is smaller.

Example B: Same limit, different balances

- Person 3: $1,800 balance on a $2,000 limit → 90% utilization

- Person 4: $300 balance on a $2,000 limit → 15% utilization

The limit didn’t change — the balance did. That’s why “balance management” is usually the fastest lever you control.

Example C: Closing a card (why the limit matters)

Closing a card can reduce your total available credit, which can raise your utilization even if your spending stays the same.

That’s one reason closing a no-fee, zero-balance card can sometimes hurt more than people expect.6

6) Simple rules to use limit & balance to your advantage

- Use the limit as a guardrail, not a goal. A higher limit doesn’t mean you should borrow more.

- Keep utilization low. Many guides use <30% as a baseline, and single digits can be even stronger for scoring.3

- Don’t carry a balance “for your score.” You generally don’t need to carry a balance to build credit; paying on time is what matters most.4

- If you’re trying to optimize utilization: pay down balances before the statement closes so the reported balance is lower.3

- Before closing a card: do the math on your new utilization first (especially if the card has no annual fee).

7) Quick FAQ

Is my balance the same as my statement balance?

Not always. Your current balance changes daily, while your statement balance is the snapshot at the end of the billing cycle.1

Do I need to carry a balance to build credit?

Usually no. You can build credit by using the card and paying on time — you generally don’t need to carry a revolving balance month to month to “help” your score.4

Which matters more for my score: limit or balance?

The score-relevant piece is usually the relationship between them (utilization).

Your balance is what you control most month to month; your limit sets the frame you operate in.

Why did my score dip if I pay in full?

It can happen if a high balance was reported during the month (often around statement closing).

Paying earlier can lower the amount that gets reported and reduce utilization next cycle.3

Sources

- Experian (Credit Terms): definitions and explanations for credit limit, statement balance/current balance, and utilization.

Open source - Capital One: credit limit definition (maximum amount you can charge on a credit card).

Open source - Experian: how utilization is calculated from reported balances, and why statement-closing timing can matter.

Open source - Consumer Financial Protection Bureau (CFPB): guidance on utilization (including the common “below 30%” guideline) and not needing to carry a balance.

Open source - myFICO: educational breakdown of FICO score categories (including “amounts owed” / utilization as a major factor).

Open source - Experian: explanation that closing an account can affect utilization (and therefore scores).

Open source - CFPB (Ask CFPB): guidance that paying your credit card balance in full each month is generally a good practice (and you don’t need to carry a balance to benefit).

Open source

Disclosure: Educational content only. Credit scoring models and lender decisions vary. Always check your card’s terms and your own credit reports for accuracy.