Quick Answer

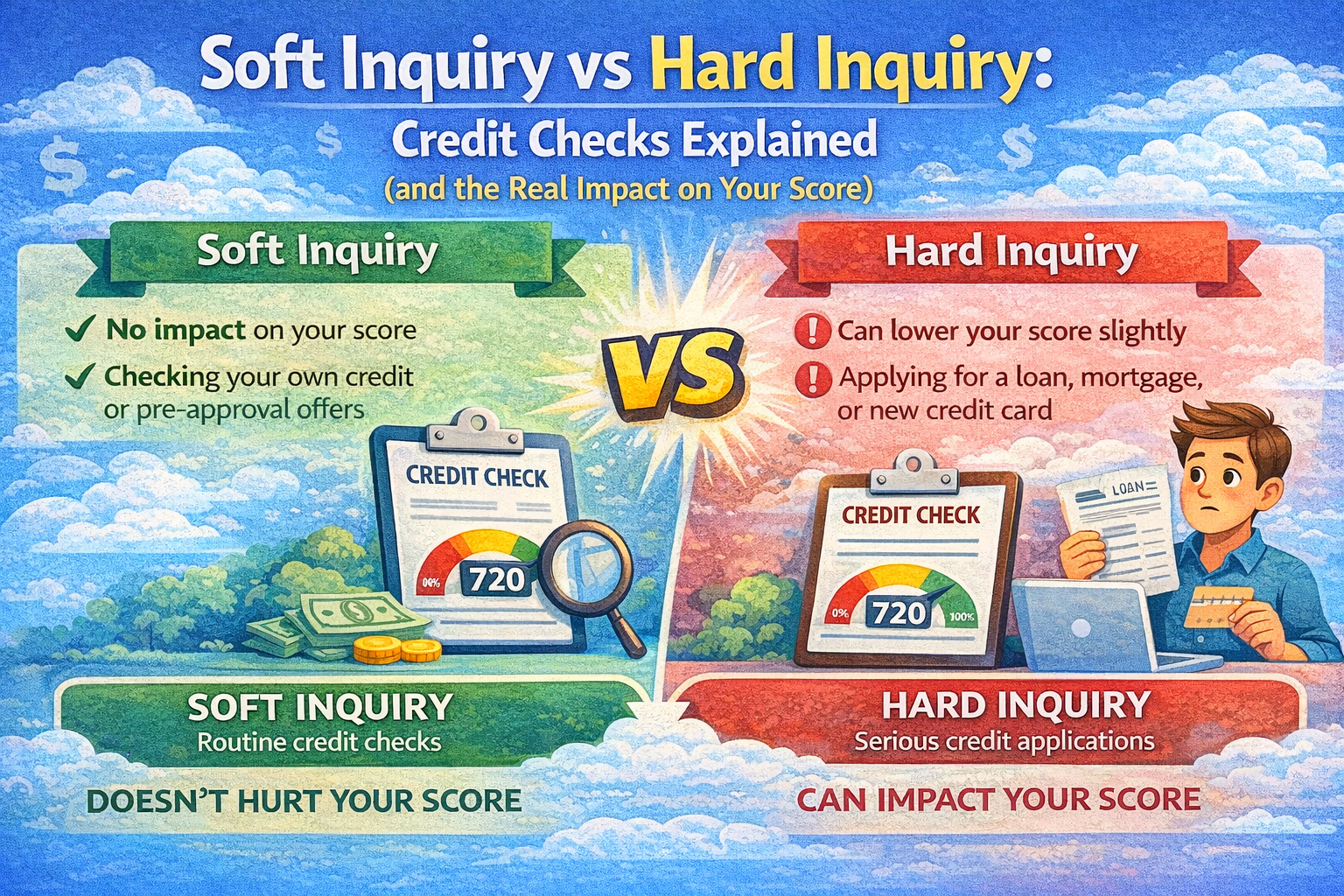

Soft inquiry (soft pull): A credit check that does not affect your credit score. Only you can see it on your report — lenders checking your file for a lending decision cannot.1

Hard inquiry (hard pull): A credit check tied to a new credit application. It can cause a small, temporary score dip and is visible to other lenders.1

Hard inquiries commonly stay on your report for up to two years, but the scoring impact is usually shorter — often around 12 months for FICO scoring.4

In 30 Seconds

- Soft pulls cover things like checking your own score, account reviews, and prescreening. No score impact.1

- Hard pulls happen when you apply for a card or loan. Usually a small, temporary dip for most people.4

- Rate shopping: do mortgage or auto loan quotes in a short window so scoring models can treat them as one inquiry.23

- Pre-qualify is often soft; the full application is often hard. Always confirm before clicking “submit.”

Where it gets more nuanced is when lenders check your credit as part of an application. That is a hard inquiry, and it can cause a small, temporary dip. Knowing which type applies — before you click submit — can be the difference between an expected score dip and an unnecessary one.

One part that surprises many beginners: comparing loan offers from multiple lenders does not have to mean multiple score hits — if you know how the rate-shopping window works.

Soft vs. Hard Inquiries: Simple Comparison

| Type | Common Reasons | Score Impact | Visible to Other Lenders? |

|---|---|---|---|

| Soft inquiry | Checking your own report or score, account reviews by existing lenders, prescreening for offers, some tenant and employment screening1 | No impact on scores1 | No — shown only to you1 |

| Hard inquiry | Applying for credit cards, auto loans, mortgages, personal loans | Usually small and temporary — often 5 points or less for many people4 | Yes — other lenders can see it1 |

What Is a Soft Inquiry?

A soft inquiry is a credit check that is not connected to a new credit application. The CFPB notes that soft inquiries do not affect credit scores and are typically shown only to you on your report — not to lenders reviewing your file.1

In simple terms: it is a look at your credit file that does not leave a mark that hurts you.

Common Examples of Soft Inquiries

- Checking your own credit report or score2

- An existing lender doing an “account review” — for example, reviewing whether to increase your credit limit3

- Prescreening — when lenders check whether you meet basic criteria before sending you a pre-approved offer in the mail1

- Some background checks for rental applications or employment (though processes vary — always confirm with the screener)

What Is a Hard Inquiry?

A hard inquiry happens when a lender checks your credit report as part of deciding whether to approve you for new credit. Unlike soft inquiries, hard pulls can have a small impact on your score and are visible to other lenders who review your report later.1

How Much Does a Hard Inquiry Lower Your Score?

For most people, not much. Experian, citing FICO guidance, notes that a single hard inquiry typically lowers a score by five points or less.4

A common mistake beginners make is assuming a hard inquiry will cause a major score drop. In most cases, the effect is small and temporary. That said, the impact can feel larger in certain situations:

- If your credit file is new or thin (not much history yet)

- If you apply for multiple types of credit in a short period

- If a rising card balance increases your utilization at the same time

How Long Do Hard Inquiries Stay on Your Report?

Hard inquiries commonly remain visible on your credit reports for up to two years. However, the scoring impact is typically shorter — often around 12 months for FICO scoring models.4

| What happens | Typical timeline |

|---|---|

| Stays visible on your credit report | Up to 2 years |

| Affects your FICO score | Often around 12 months |

| Score impact for most people | 5 points or less per inquiry |

Timelines above reflect commonly cited guidance from Experian and FICO. Exact impact varies by scoring model, version, and individual credit profile.4

Rate Shopping (Auto and Mortgage): How to Avoid Multiple Hits

When you are comparing loan offers from multiple lenders, each lender may run a hard inquiry. Credit scoring models are generally designed to recognize when you are shopping for a single loan — grouping multiple inquiries into one if they happen within a short window.

Mortgages

The CFPB explains that if multiple mortgage lenders check your credit within a short window — commonly cited as 45 days — those checks may be counted as a single inquiry for scoring purposes.2

Auto Loans

For auto loan shopping, the CFPB notes that multiple checks within a short time window may also count as a single inquiry. Depending on the scoring model, that window can range from 14 to 45 days.3

What This Means in Practice

- Comparing three mortgage lenders within one week: likely treated as one inquiry

- Comparing three mortgage lenders spread across three months: likely treated as three separate inquiries

- The exact window varies by scoring model — 14 days is a conservative estimate that works across most3

Note: Rate-shopping grouping applies to mortgage and auto loans. It does not apply to credit card applications — each credit card application is typically counted as a separate hard inquiry regardless of timing.5

Pre-Qualification vs. Pre-Approval: Soft or Hard?

Many lenders offer a “pre-qualify” or “check your rate” step before you submit a full application. In many cases, this initial step uses a soft inquiry — meaning it will not affect your score. The hard inquiry typically happens only when you move forward with a full application.1

The problem is that not every lender follows this pattern, and the labels “pre-qualify” and “pre-approval” are not standardized. One lender’s “pre-approval” might be a soft pull; another’s might be a hard pull.

Before you make a decision, ask these questions directly — before clicking submit:

No-Surprises Checklist

- “Is this a soft inquiry or a hard inquiry?”

- “Will this affect my credit score?”

- “Is this a pre-qualification or a full application?”

- “If I am comparing loan offers, does rate-shopping grouping apply — and what is the window?”

If You See a Hard Inquiry You Do Not Recognize

- Pull your credit reports and look at the inquiries section. In the U.S., the official source for free reports is AnnualCreditReport.com.2

- Identify the company that ran the inquiry and look up their official contact information independently — not from any link in an unexpected email.

- Contact the company directly and ask why they accessed your report. Mistakes do happen, and sometimes a pull can be disputed.

- Check for new accounts you did not open. An unfamiliar inquiry alongside an unfamiliar account is a stronger signal of fraud.

- If you suspect fraud, file a dispute with the credit bureau(s) and consider two protective options:

- Fraud alert: Tells lenders to take extra steps to verify your identity before opening new credit in your name. Free to place and lasts one year.

- Credit freeze: Blocks lenders from accessing your credit report entirely until you lift it. Free to place and remove — and the strongest protection against new accounts being opened in your name without your knowledge.

The CFPB provides step-by-step guidance for both options at consumerfinance.gov.

FAQ

Does checking my own credit hurt my score?

No. Checking your own credit report or score is a soft inquiry and has no effect on your score. This applies whether you check through a free monitoring service, your bank’s app, or directly through the bureaus.2

How long do hard inquiries stay on my report?

Hard inquiries commonly remain visible on your credit reports for up to two years. The scoring impact, however, is usually shorter — often around 12 months for FICO scoring models. After that point the inquiry is still listed but no longer affects calculations.4

How many hard inquiries is “too many”?

There is no universal cutoff number. Context matters as much as count. Applying for three credit cards in one month looks different to lenders than shopping three mortgage rates in one week — even if the raw inquiry number is the same. The first pattern can signal financial stress; the second signals responsible comparison shopping. As a rough guide, more than two or three unrelated hard inquiries within a few months can become a visible pattern on your report. Rate-shopping inquiries that fall within the grouping window are the main exception to that rule.23

Can landlords or employers cause a hard inquiry?

Many tenant and employment screenings use soft inquiries — but practices vary by company and location. Some people assume all background checks are soft pulls, which is not always accurate. The safest approach is to ask the screener directly: “Will this be a hard or soft inquiry on my credit?”1

Does a hard inquiry affect FICO and VantageScore the same way?

Both scoring models consider hard inquiries, but they weigh them slightly differently and may use different time windows when grouping rate-shopping inquiries. The general principle — that a single hard inquiry has a small, temporary impact — applies to both, but exact details vary by model and version.4

Can I dispute a hard inquiry I did not authorize?

Yes. If a hard inquiry appears on your report and you did not authorize it, you can dispute it with the credit bureau that shows it. The CFPB provides consumer guidance on the dispute process. Unauthorized inquiries are worth investigating since they can indicate fraud.1

What to Do Next

Start by pulling your free credit reports from AnnualCreditReport.com and checking the inquiries section. Look for anything you do not recognize — an unfamiliar hard inquiry is worth a quick investigation, even if it turns out to be harmless.

Going forward, the single most useful habit is asking one question before any credit check: “Is this a soft or hard inquiry?” Most lenders will tell you. For loan shopping specifically — mortgages and auto loans — keeping your comparisons within a short window means the inquiries are more likely to be grouped as one rather than counted separately.

Soft pulls give you information at no cost to your score. Use them freely. Reserve hard pulls for when you are ready to actually move forward with an application.

References

-

CFPB. “What is a credit inquiry?” — defines soft vs. hard inquiries; visibility to lenders; score impact distinction.

Source -

CFPB. “What exactly happens when a mortgage lender checks my credit?” — mortgage rate-shopping window; checking your own credit; report basics.

Source -

CFPB. “I am shopping for a car and applying for an auto loan. Will lenders pull multiple credit inquiries?” — rate-shopping window for auto loans; window varies by model (14–45 days).

Source -

Experian. “Credit Checks: What are credit inquiries?” — typical point impact; how long inquiries stay on report; FICO vs. VantageScore timing notes.

Source -

myFICO. “How do inquiries affect your FICO Score?” — confirms rate-shopping grouping applies to mortgage and auto loans but not credit card applications; scoring impact and window details.

Source

Disclosure: This article is general education, not financial advice. Credit scoring, lender criteria, and reporting practices vary by bureau, lender, product, and time.