Not all credit checks are equal. Here’s what counts as a soft pull, what counts as a hard pull, how much it usually matters,

and how to rate-shop (auto/mortgage) without getting dinged multiple times.

Quick answer (snippet-friendly)

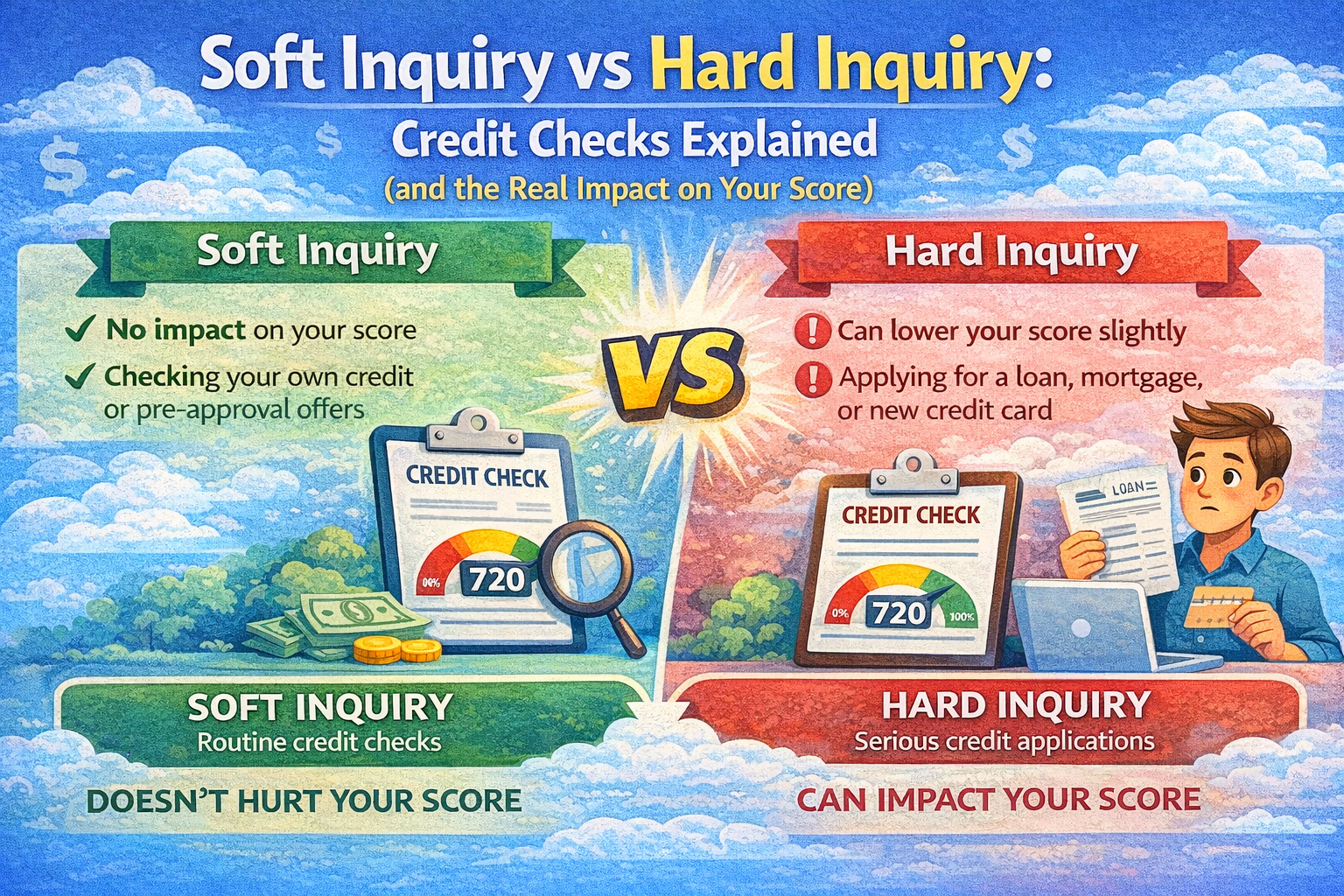

Soft inquiry (soft pull): A credit check that does not affect your credit scores and is

typically shown only to you on your report.1

Hard inquiry (hard pull): A credit check tied to an application for new credit.

It can cause a small, temporary score drop and is visible to lenders.1

Timeline basics: hard inquiries commonly remain visible on your reports for up to two years, but scoring impact

is usually shorter (often about 12 months for FICO scoring).4

Soft vs. hard inquiries (simple comparison)

| Type | Common reasons | Score impact | Visible to lenders? |

|---|---|---|---|

| Soft inquiry | Checking your own report/score, account reviews, prescreening, some tenant/employment screening 1 |

No impact on scores1 | Generally no (shown only to you)1 |

| Hard inquiry | Applying for credit cards, auto loans, mortgages, personal loans | Usually small & temporary (often ≤ ~5 points for many people)4 | Yes, other lenders can see it1 |

Many tools start soft and become hard only when you submit a full application—but not all.

What is a soft inquiry?

A soft inquiry is a credit check that’s not tied to a new-credit application decision.

The CFPB notes soft inquiries don’t affect credit scores and are typically shown only to you.1

Common soft inquiry examples

What is a hard inquiry?

A hard inquiry typically happens when you apply for new credit and a lender checks your report to make an approval/terms decision.

It can have a small impact on scores and is visible to other lenders.1

How many points does a hard inquiry lower your score?

Often not much. Experian (citing FICO guidance) notes a single hard inquiry typically lowers scores by

five points or less for many people.4

How long do hard inquiries stay on your report?

Hard inquiries commonly remain on your credit reports for up to two years,

though scoring impact is usually shorter (often about 12 months for FICO).4

if you stack multiple applications, or if your utilization rises at the same time.

Rate shopping (auto & mortgage): how to avoid “multiple hits”

Credit scoring models often try to recognize you’re shopping for one loan and may group multiple inquiries if they happen within a short window.

Mortgages

The CFPB explains that if multiple mortgage lenders check your credit in a short window (commonly cited as 45 days),

the checks may be recorded as a single inquiry for scoring purposes.2

Auto loans

The CFPB notes that for auto loan shopping, multiple checks may count as a single inquiry if made within a short time window,

and that the window can range from 14 to 45 days depending on the scoring model.3

“Pre-qualification” vs “pre-approval”: soft or hard?

Many “pre-qualify” or “check your rate” steps are soft inquiries at the quote stage, and then become hard inquiries when you submit a full application.

Don’t guess—confirm before proceeding.

No-surprises checklist (copy/paste)

- “Is this a soft inquiry or a hard inquiry?”

- “Will this affect my credit score?”

- “Is this pre-qualification or a full application?”

- “If it’s a loan, does rate shopping apply—and what window?”

If you see a hard inquiry you don’t recognize

- Pull your credit reports and review the inquiries/access list (use the official report source if you’re in the U.S.).2

- Contact the company using official contact info and ask why they accessed your report.

- Check for any new accounts you didn’t open.

- If you suspect fraud, dispute with the bureau(s) and consider a fraud alert or credit freeze (process varies by country/state).

FAQ (snippet-friendly)

Does checking my own credit hurt my credit?

No. Checking your own credit is typically a soft inquiry and doesn’t affect scores.2

How long do hard inquiries stay on my report?

Commonly up to two years, but scoring impact is usually shorter (often ~12 months for FICO).4

How many hard inquiries is “too many”?

There’s no universal number, but multiple hard pulls close together can signal higher risk. For auto/mortgage, keep inquiries inside the rate-shopping window.23

Can landlords or employers cause a hard inquiry?

Many tenant/employment screenings are soft inquiries, but processes vary. Ask the screener directly: “Will this be a hard or soft inquiry?”1

References

- Consumer Financial Protection Bureau (CFPB). “What is a credit inquiry?” (defines soft vs hard inquiries; visibility; score impact distinction).

- CFPB. “What exactly happens when a mortgage lender checks my credit?” (mortgage rate-shopping window; checking your own credit; report basics).

- CFPB. “I am shopping for a car and applying for an auto loan. Will lenders pull multiple credit inquiries?” (rate-shopping window varies by model; often 14–45 days; related guidance).

- Experian. “Credit Checks: What are credit inquiries?” (typical point impact; how long inquiries stay; FICO vs VantageScore timing notes).

Mrhamza:

Research-focused writing built from primary consumer/regulator sources and updated when guidance changes.