Utilization can move your score even when you pay on time—because scores react to the balances that get reported.

Disclosure: Educational only, not financial advice.

Quick answers

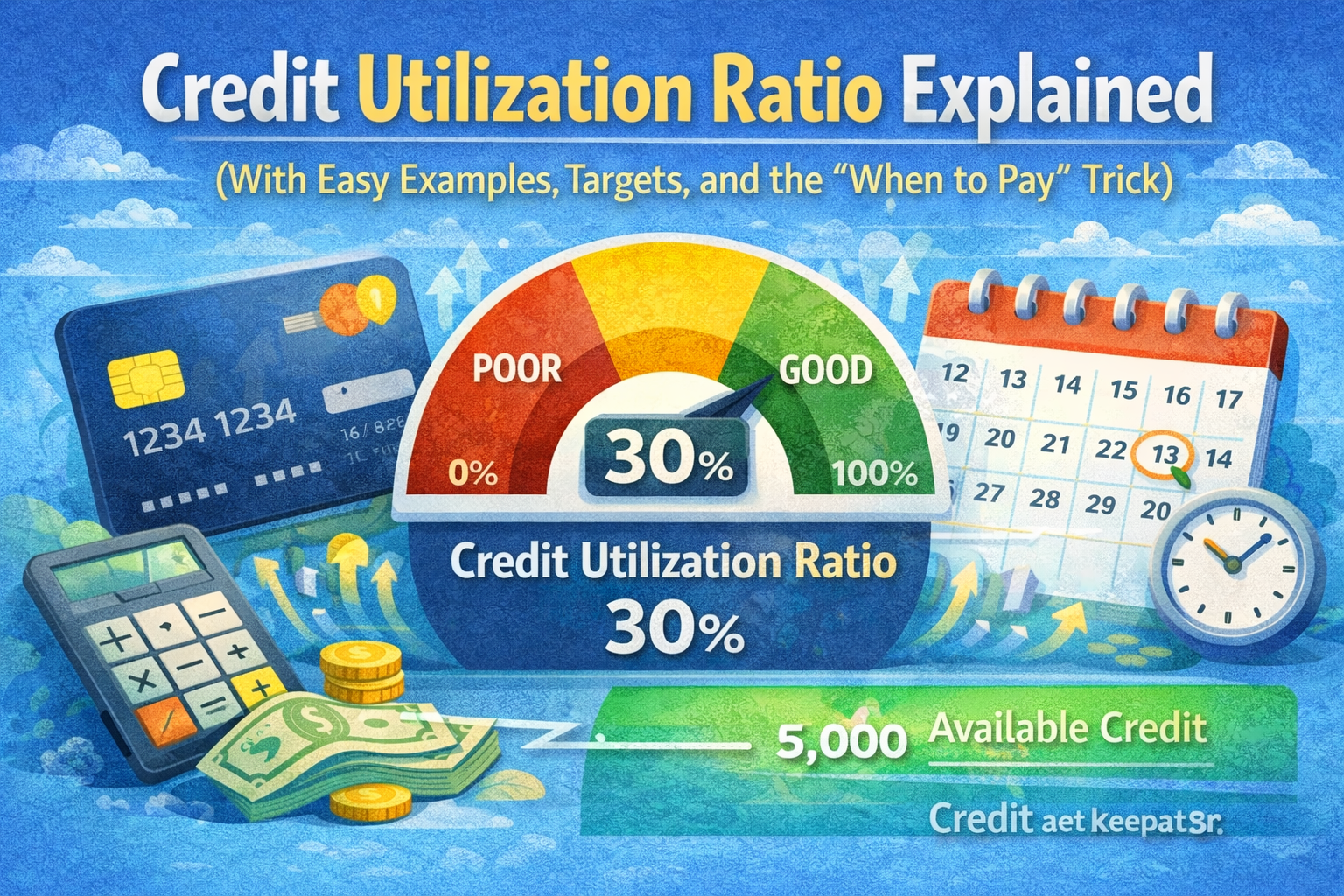

- Utilization = (reported revolving balances ÷ revolving limits) × 100 1

- Scores look at overall utilization and per-card utilization. 2

- A common guideline is below ~30%; stronger profiles often keep utilization under 10%. 2

- To reduce what shows on your reports fast, pay before your statement closing date (reporting is often near that date). 2

- Checking your own credit typically won’t lower your scores. 2

Why it matters

Utilization is part of the “amounts owed” category and is a major scoring input—high utilization can look risky, especially if one card is near its limit. 1

Best habit: keep any card from reporting high

Applying soon: aim low single digits

What is credit utilization?

Credit utilization is the percentage of your available revolving credit you’re using—mainly credit cards and lines of credit.

It’s calculated from the balances and limits that appear on your credit report. 1

How to calculate utilization (2 ways)

1) Overall utilization

Example

| Card | Reported balance | Limit | Utilization |

|---|---|---|---|

| Card A | $500 | $2,000 | 25% |

| Card B | $300 | $1,000 | 30% |

| Card C | $0 | $2,000 | 0% |

| Total | $800 | $5,000 | 16% |

2) Per-card utilization

Why this matters: you can have “fine overall utilization” while one card reports very high and drags scores down. 2

What utilization should you aim for?

There’s no magic number that guarantees approval, but practical targets are well-established:

many experts suggest staying below ~30% to avoid significant score reductions, while people with exceptional scores often keep utilization under 10%. 2

| Goal | Overall target | Per-card target | What it signals |

|---|---|---|---|

| Building / staying safe | < 30% | < 30% | Lower risk profile vs high utilization |

| Stronger scoring habits | < 10% | < 10% | Typical of top-tier score behavior |

| Applying soon (30–45 days) | Low single digits | Avoid any card “high” | Minimizes “maxed-out” signals right before underwriting |

The best time to pay (the biggest lever)

Why paying on the due date can still show high utilization

Credit scores react to the balance that gets reported. Many lenders report on their own schedules, and the balance reported is often the amount outstanding

on or near your statement closing date—not your payment due date. 2

The strategy

To lower reported utilization quickly, pay the balance down before the statement closes so a smaller number is reported. 2

How to find your statement closing date

- Open your last statement PDF (or your issuer app’s “Statements” section)

- Look for Statement Closing Date

- Set a reminder 3–5 days before (time for payments to post)

Simple example (why it works)

Limit: $500

You spend: $450

If $450 reports → utilization = 90%

If you pay $400 before close, $50 reports → utilization = 10%

Fast ways to lower utilization (ranked by speed)

- Pay before statement close (fastest next-cycle change). 2

- Two payments per month (mid-cycle + pre-close) to prevent high reporting. 2

- Spread spending so no single card reports high.

- Request a credit limit increase (only if spending stays stable). 2

- Check for reporting errors (wrong limit/balance can inflate utilization).

FAQ

Does utilization reset every month?

It can change quickly because new balances are reported regularly. That’s why paying before the statement closing date can show improvement faster than many other credit factors. 2

Should I focus on overall utilization or per-card utilization?

Both. Overall matters, but one card reporting very high can still look risky. 2

Does checking my utilization hurt my score?

Checking your own credit generally won’t lower your scores. 2

Where can I check my credit reports for free?

The FTC notes you can get free reports via AnnualCreditReport.com, and the bureaus have permanently extended free weekly reports through that site. 3

Conclusion

Utilization is simple math, but timing matters. If you want the quickest next-cycle improvement:

pay down balances before your statement closing date so the reported balance stays low—and avoid any single card reporting “near max.” 2

References

Mrhamza:

Money basics writer • Credit scores, reports, and everyday finance explainers

Research-focused writing built from primary consumer/regulator sources and updated when guidance changes.