What they do, how they differ, and when a fraud alert may be the better fit.

Quick answer

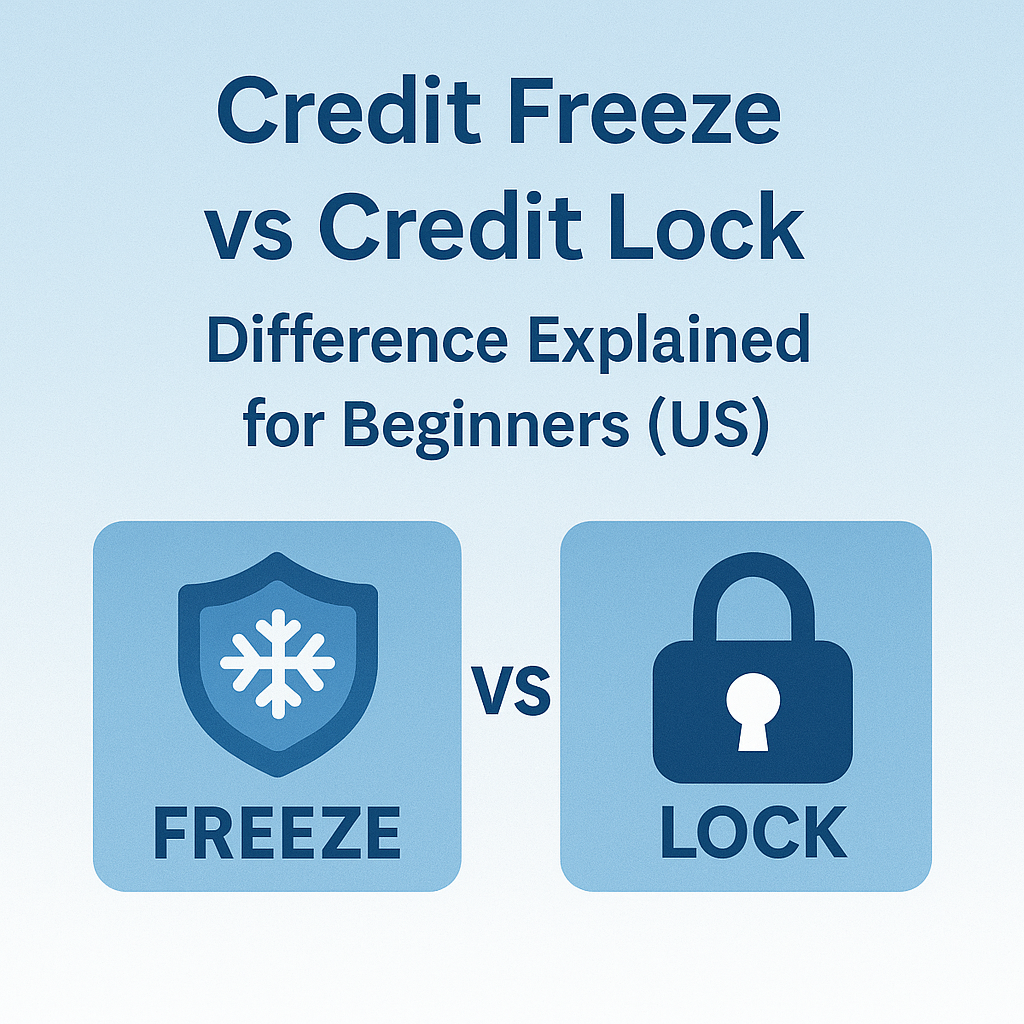

Credit freeze (security freeze): a free, legal-right tool that restricts access to your credit report to help stop new accounts from being opened in your name.1

Credit lock: a bureau/app feature that works similarly, but it’s a product/feature with provider terms. The CFPB notes locks are no more effective than freezes (which are free and a right by law).1

1) The one-glance difference

| Feature | Credit Freeze (Security Freeze) | Credit Lock |

|---|---|---|

| Cost | Free to place and lift1 | Depends on provider/plan; not required to be free1 |

| Legal protections | Backed by federal law (“right by law”)1 | Provider terms/feature; not “more effective” than a freeze1 |

| What it does | Restricts access to your report for new credit checks2 | Similar goal (restrict access) but depends on the service implementation1 |

| Setup | You place it with each bureau (Equifax, Experian, TransUnion)2 | Also provider/bureau-by-bureau; usually managed in an app/portal |

| Credit score impact | No impact (it controls access, not your data)2 | No impact (same reason) |

2) What is a credit freeze?

A credit freeze (also called a security freeze) restricts access to your credit report. When lenders can’t access your report, they typically can’t open new credit in your name—so it’s a strong step against new-account identity theft.2

A freeze does not stop activity on accounts you already have, and it doesn’t prevent every type of identity theft (for example, tax or benefits fraud). It mainly targets new credit openings.2

3) What is a credit lock?

A credit lock is a bureau/provider feature that also restricts access to your credit report for new credit checks. The CFPB’s key point is practical:

credit locks are no more effective than security freezes—and freezes are free and a right by law.1

4) Special case: protecting a child’s credit

The FTC explains that parents/guardians can place a free credit freeze for a child (and for other protected individuals) by contacting each bureau and following their minor-freeze process.2

5) Where does a fraud alert fit?

A fraud alert is different: it doesn’t block access to your report. Instead, it signals lenders to take extra steps to verify identity before issuing new credit.2

- Initial fraud alert: typically lasts 1 year.2

- Extended fraud alert: can last 7 years if you’re an identity theft victim and provide the required documentation.2

- The FTC notes that you can place an alert with one bureau, and it has a process to notify the others.2

6) When to use freeze vs lock vs fraud alert

Choose a credit freeze when:

- You want strong new-account protection as a default.

- You were in a breach involving sensitive info (like SSN), or you see suspicious activity.

- You’re protecting a child’s credit file.2

Choose a credit lock when:

- You specifically want the provider’s app workflow/features and you’re okay with the provider’s terms.

- You understand it’s not “more protective” than a freeze.1

Consider a fraud alert when:

- You still need to apply for credit soon and don’t want to thaw a freeze repeatedly.

- You want extra verification friction for lenders without fully blocking access.2

7) How to place a credit freeze (high level)

- Place a freeze with each major bureau (Equifax, Experian, TransUnion).2

- Save your logins/confirmation details so you can lift the freeze when needed.

- Before applying for credit, lift (thaw) the freeze temporarily (date window) or per-bureau as required.

8) If you see an inquiry or account you don’t recognize

- Pull your credit reports and look for unfamiliar inquiries/accounts.

- Contact the company using official contact info (not the phone number in a suspicious email).

- If identity theft is possible, use FTC’s identity theft resources and consider freezing your reports immediately.2

9) Quick FAQ

Do freezes or locks hurt my credit score?

No. They control access to your report; they don’t change the data used to calculate scores.2

If I freeze my credit, can I still use my existing accounts?

Yes. A freeze is aimed at new credit checks; it doesn’t stop you from using existing credit cards/loans.2

Is a lock stronger than a freeze?

No. The CFPB says locks are no more effective than freezes, and freezes are free and a right by law.1

Educational note: This guide is general information only and isn’t legal or financial advice. Policies and processes can vary by bureau and by product.

References

- Consumer Financial Protection Bureau (CFPB) — “Credit Locks & Credit Freezes” (locks are no more effective than freezes; freezes are free and a right by law).

Source

↩ - Federal Trade Commission (FTC) — “Credit freezes and fraud alerts” (what freezes do; fraud alert basics; 1-year initial alerts; 7-year extended alerts; minor freeze info).

Source

↩ - TransUnion — Member Help Center (credit lock feature status; “free option that works just as well—a credit freeze”; freeze is free to freeze/unfreeze/lift).

Source

↩