Quick Answer

Average Age of Accounts (AAoA) is the average length of time all your credit accounts have been open. It is one of the factors inside the “length of credit history” category used in most credit scoring models. FICO educational materials describe length of credit history as making up roughly 15% of a FICO Score — and AAoA is one of several age-related signals within that category.1

- Opening a new account lowers AAoA because every new account starts at zero months old

- Closing an old account does not always hurt AAoA immediately — closed accounts can stay on your report for years and may still count toward age calculations.2

- The bigger short-term risk when closing a card is often utilization — not age

Average Age of Accounts, often shortened to AAoA, is how old your credit accounts are on average. A longer history can signal to lenders that you have managed credit over time. A shorter one — especially when it drops suddenly — can raise a flag, even if nothing else changed.

The part that trips up most beginners: AAoA does not just move slowly upward on its own. It can drop sharply the moment you open a new account. And it does not always drop when you close one.

What Counts in AAoA?

AAoA is calculated using the accounts that appear on your credit reports. This typically includes:

- Credit cards and lines of credit (called revolving accounts — you can borrow, repay, and borrow again)

- Installment loans — auto loans, student loans, mortgages, and personal loans (a fixed amount borrowed and repaid in regular payments)

Whether scoring models include only open accounts, or both open and closed accounts that still appear on your report, can vary. The practical point holds either way: older, well-managed accounts generally help your length of credit history.1

Why AAoA Affects Your Score

AAoA is not scored as a standalone category. It is one signal inside the broader “length of credit history” category, which FICO educational materials describe as making up roughly 15% of a FICO Score.14

Within that category, scoring models typically look at several age-related signals together:

| Signal | What it reflects |

|---|---|

| Oldest account age | How long you have had credit at all |

| Newest account age | How recently you opened something new |

| Average age of accounts (AAoA) | The overall maturity of your credit profile |

Source: myFICO educational materials.1 Exact weighting varies by scoring model and version.

Because length of credit history is 15% of your FICO Score — versus 35% for payment history and 30% for amounts owed — it matters, but it is not the biggest lever. Beginners often worry too much about AAoA and not enough about payment history and utilization.

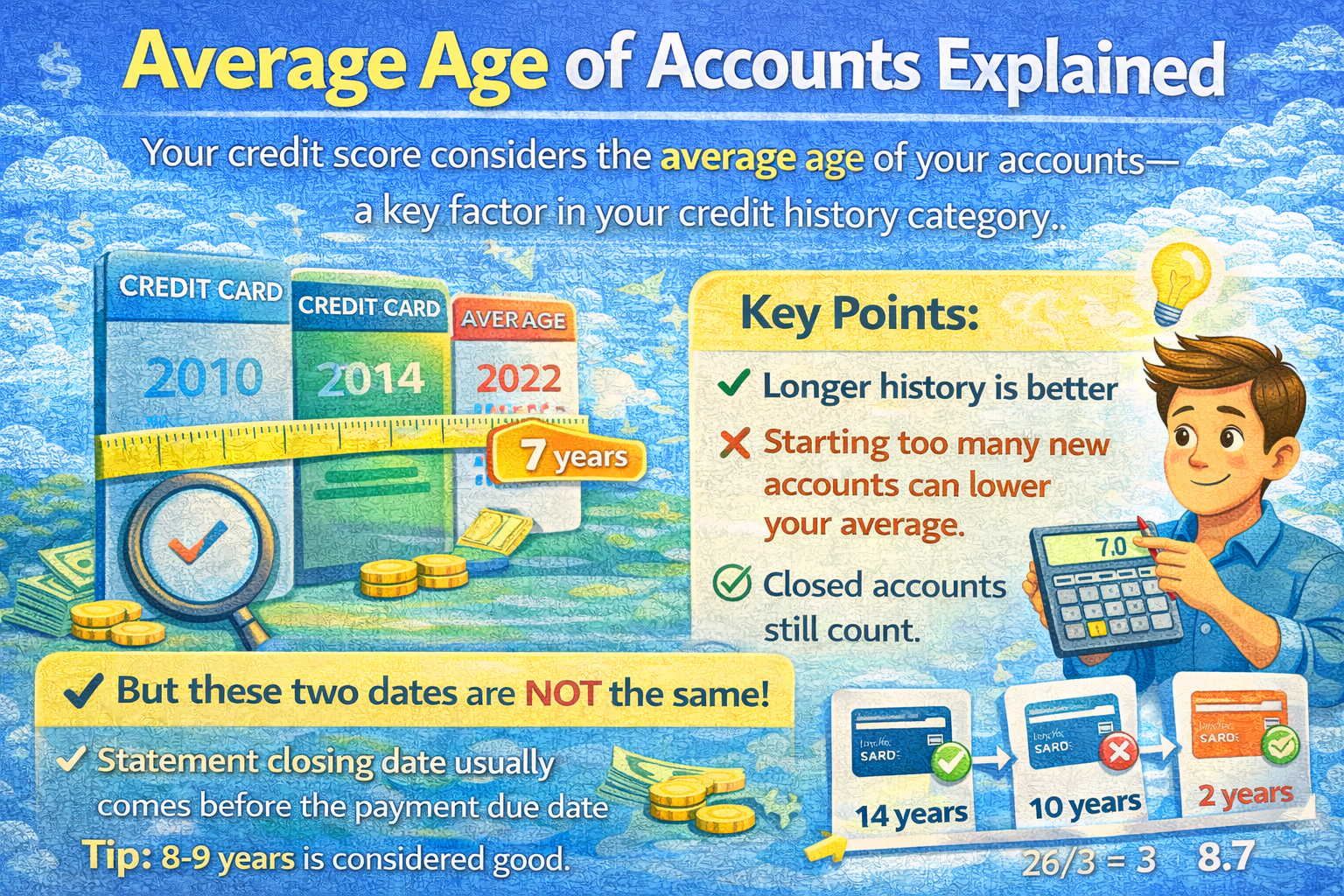

How to Calculate Your AAoA

The math is straightforward. You do not need a special tool.

- List every account on your credit report

- Calculate how many months old each one is (months since the account was opened)

- Add all the months together

- Divide by the total number of accounts

Worked Example (as of February 2026)

| Account | Opened | Age in months |

|---|---|---|

| Card A | Feb 2022 | 48 months |

| Card B | Feb 2024 | 24 months |

| Loan C | Feb 2025 | 12 months |

| Total | 84 months |

AAoA = 84 ÷ 3 = 28 months (2 years, 4 months)

Mini AAoA Calculator

Enter each account’s age in months — one per line — then click Calculate.

What Happens When You Open a New Account?

Every new account starts at zero months old. Because AAoA is a simple average, adding a zero to the calculation pulls the result down — every time, without exception. This is just basic math, not a penalty the system applies to you.

Continuing the example above

Original AAoA with 3 accounts: 28 months

| Account | Age in months |

|---|---|

| Card A | 48 |

| Card B | 24 |

| Loan C | 12 |

| New Card D | 0 |

| New AAoA | 84 ÷ 4 = 21 months |

One new account dropped AAoA from 28 months to 21 months — a 7-month decrease instantly.

Does Closing a Credit Card Hurt AAoA?

Closing an account does not immediately erase it from your credit report. Closed accounts — especially those with positive history — can remain visible on your report for years after closing.23 While they are still on your report, many scoring explanations treat them as still contributing to age calculations.1

In simple terms: a closed card does not vanish from your credit history on the day you close it. Its age continues to count while it stays on your report.

When closing a card does create a problem

The more immediate risk when closing a card is usually credit utilization — not account age. Here is why:

- Closing a card removes its credit limit from your total available credit

- If you carry balances on other cards, your total utilization percentage goes up

- Utilization is a faster-moving score factor than age for most people — and a higher utilization can cause a more immediate score drop

When the age impact does eventually show up

If you close your oldest account and it eventually falls off your credit report entirely, both your oldest account age and your AAoA can drop. This can happen years later — not immediately. The timing depends on the bureau and account type.23

How to Protect Your AAoA

AAoA cannot be rushed — but it can be protected. Here are practical approaches based on where you are with credit.

If you are building credit from scratch

- Open fewer accounts to start — each one pulls the average down

- Choose accounts you intend to keep long-term, even after you no longer actively use them

- Focus first on payment history and low utilization — those move scores faster than age does

If you want better card benefits without a score hit

- Ask your card issuer about a product change — this means requesting to switch your existing card to a different card product within the same bank (for example, converting a no-rewards card to a cash-back card), without closing the account. Because the account stays open rather than being replaced, the original open date is often preserved. Rules vary by bank and card type, so confirm the terms before requesting one.

If a major credit application is coming up

- Avoid opening new accounts in the months before applying for a mortgage, auto loan, or apartment — each new account lowers AAoA and adds a hard inquiry

- Keep your payment history clean and utilization steady in the lead-up period

- Avoid closing cards with large limits before applying — the utilization impact can be more immediate than any age effect

Common Myths About AAoA

| Myth | What is actually true |

|---|---|

| “Never open a new account — it will ruin your score.” | New accounts can be useful and the AAoA dip is usually temporary. The question is whether the timing and purpose make sense for your situation. |

| “Closing a card instantly wipes out its age.” | Closed accounts can stay on your report for years — see the closing section above for the full explanation.2 |

| “AAoA is the only age signal that matters.” | Length of credit history also looks at your oldest account age and your newest account age — not just the average.1 |

| “A higher AAoA always means a higher score.” | AAoA is one factor among many. Payment history and utilization carry more weight for most people. A long history with missed payments still hurts. |

FAQ

Does AAoA include loans or just credit cards?

AAoA is typically based on all the accounts that appear on your credit reports — both revolving accounts (like credit cards and lines of credit) and installment accounts (like auto loans, student loans, and mortgages). The exact accounts included can vary by scoring model.

How fast can AAoA improve?

Slowly — time is the only input. Your AAoA rises automatically as each month passes with no new accounts added.

A rough example: if you open a new card today and your AAoA drops from 36 months to 24 months, it takes approximately 12 months of no new accounts before AAoA climbs back to 36 — because all existing accounts age together during that window. The more accounts you already have, the smaller the drop from one new card, and the faster the recovery.

The fastest way to let AAoA recover is to stop opening new accounts and let time do the work. There is no shortcut.

Will opening a new card lower my score even if I never use it?

It can. Opening a new account lowers AAoA and adds a hard inquiry — both of which can affect your score temporarily. Whether you use the card or not does not change the age math. That said, the effect is often short-lived if your payment history and utilization stay strong.

If I close my oldest card, does my credit history restart?

No. Closing your oldest card does not immediately erase its age — the account typically stays on your report for years after closing. The impact shows up much later, if the account eventually falls off your report entirely.23 See the closing section above for the full breakdown.

How much does AAoA actually affect my score?

AAoA is one signal within the length of credit history category, which makes up roughly 15% of a FICO Score.14 That 15% is shared across several age-related signals — oldest account, newest account, and AAoA. So the direct weight of AAoA alone is a portion of that 15%. Payment history (35%) and amounts owed including utilization (30%) have a larger impact for most people.

Should I keep a card open just to protect AAoA?

That depends on the full picture. Keeping a card open with no annual fee and low utilization generally costs nothing and preserves both the account age and the available credit limit. A card with a high annual fee that you no longer use is a different calculation. Before you make a decision, check the utilization impact of closing it — that is usually the more pressing concern than age.

What to Do Next

Start by pulling your free credit report from AnnualCreditReport.com and listing the open date for each account. Run the simple calculation in this article to see where your AAoA currently stands — and which accounts are anchoring it.

From there, the most useful habit is thinking about timing before you open or close anything. A new account opened for a good reason at the right time is worth a temporary AAoA dip. A card closed just before a mortgage application could hurt utilization more than most people expect.

AAoA grows on its own as long as you manage your existing accounts well. Before opening or closing anything, run the AAoA calculation from this article and check your utilization impact first — those two checks take five minutes and cover the most common mistakes.

References

-

myFICO (FICO education). “Should I close my credit cards?” — length of credit history ~15% of FICO Score; age metrics can include open and closed accounts while they appear on reports.

Source -

Experian. “Closing a Credit Card: Will It Hurt Your Credit?” — closed accounts can remain on reports for years; positive history can remain longer than negative.

Source -

TransUnion. “How Long Do Closed Accounts Stay on Your Credit Report?” — closed accounts may remain on reports; timelines differ for positive vs. negative history.

Source -

Consumer Financial Protection Bureau (CFPB). “What is a credit score?” — covers the factors used in credit scoring, including length of credit history.

Source

Disclosure: This article is general education, not financial advice. Credit scoring models and credit bureau reporting timelines vary by model, version, and lender.