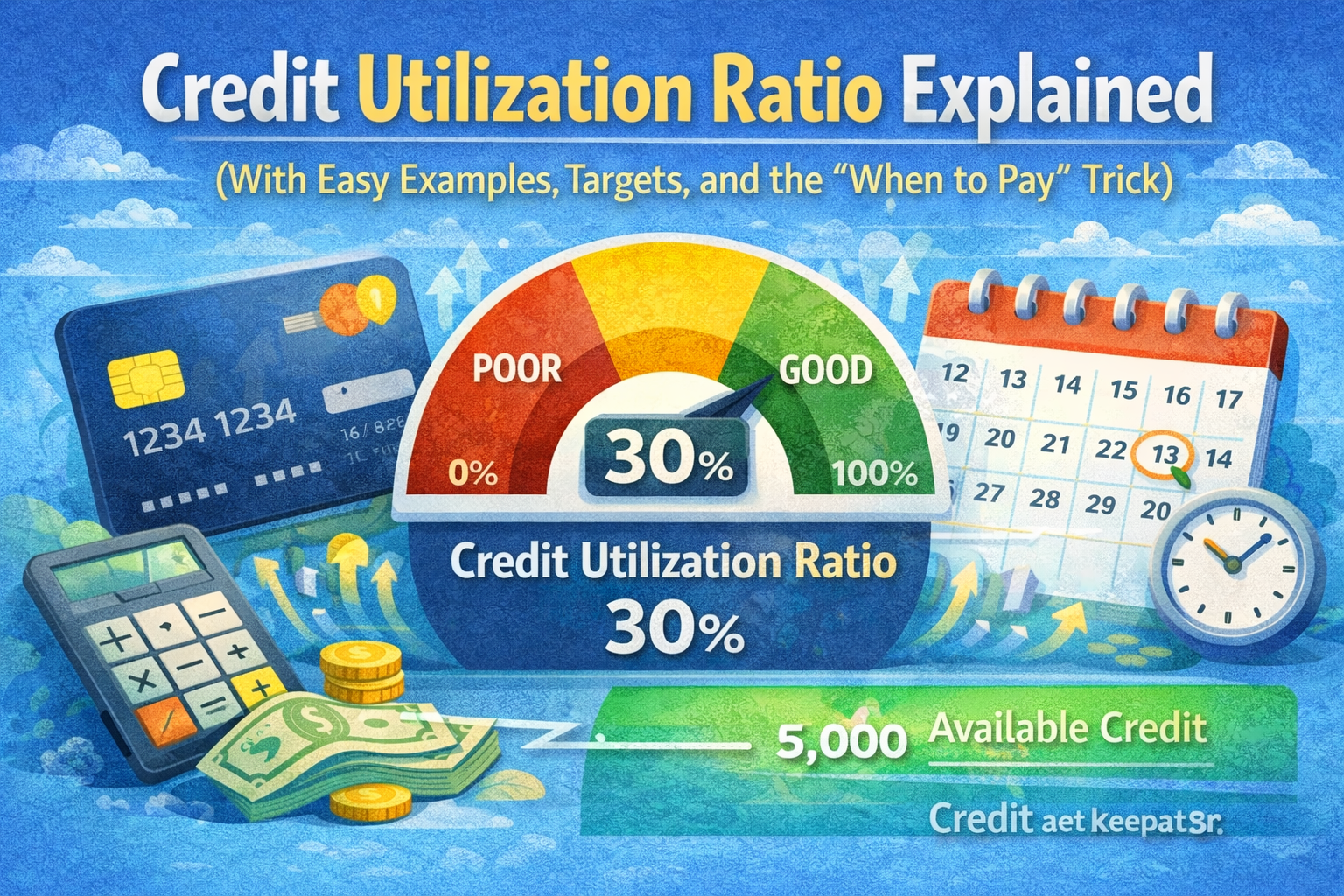

Quick Answer

Credit utilization is the percentage of your credit card limit you are currently using. If your card has a $1,000 limit and your reported balance is $300, your utilization is 30%. Keeping this number low — often below 30%, and lower when possible — can help your score because utilization is one of the more responsive credit factors. The key timing trick: pay your balance down before your statement closing date, not just by the due date.

Key Takeaways

- Utilization = (reported revolving balances ÷ revolving limits) × 100 1

- Scores look at overall utilization and per-card utilization — both matter. 2

- A common guideline is below 30%; stronger profiles often keep it under 10%. 2

- To reduce what shows on your reports fast, pay before your statement closing date. 2

- Checking your own credit does not lower your score. 2

That is credit utilization — and the timing of when you pay matters more than most people expect. This article explains what utilization is, how it is calculated, what a reasonable target looks like, and one simple habit that can make a noticeable difference.

1) What Is Credit Utilization?

Credit utilization is the percentage of your available revolving credit that you are currently using. Revolving credit refers mainly to credit cards and personal lines of credit — accounts where you can borrow, repay, and borrow again.1

In simple terms: if your credit card has a $1,000 limit and your reported balance is $400, you are using 40% of that card’s available credit. That 40% is your utilization on that card.

It is calculated from the balances and limits that appear on your credit report — not from your real-time spending. That distinction matters, and it is explained in the next section.

2) How to Calculate Utilization (2 Ways)

There are two levels of utilization that scoring models look at. A common mistake beginners make is only tracking the overall number while ignoring individual cards.

Method 1: Overall Utilization

This adds up all your reported balances and divides them by all your combined credit limits.

Example:

| Card | Reported Balance | Limit | Per-Card Utilization |

|---|---|---|---|

| Card A | $500 | $2,000 | 25% |

| Card B | $300 | $1,000 | 30% |

| Card C | $0 | $2,000 | 0% |

| Total | $800 | $5,000 | 16% overall |

Method 2: Per-Card Utilization

This is where many beginners get caught off guard. You can have a perfectly fine overall utilization rate while one individual card is reporting at 80% or 90%. That single card can still drag your score down.2

3) What Utilization Should You Aim For?

There is no single number that guarantees a certain score or an approval. Utilization is just one piece of a larger picture. That said, some well-established patterns are worth knowing about.2

| Situation | Overall Target | Per-Card Target | What It Signals |

|---|---|---|---|

| Building or staying safe | < 30% | < 30% | Lower risk compared to high utilization |

| Stronger scoring habits | < 10% | < 10% | Typical pattern among top-tier scores |

| Applying soon (30–45 days out) | Low single digits | Avoid any card reporting high | Reduces “near limit” signals before a lender reviews your file |

Before you make a decision about how much to pay down, keep in mind that utilization is just one factor. Payment history, account age, and other elements also affect scoring. This table reflects general patterns, not guarantees.

4) The Best Time to Pay (The Biggest Lever)

Why Paying on the Due Date Can Still Show High Utilization

Paying on time does not automatically mean your reported balance will be low.

Most lenders report your balance to the credit bureaus on or near your statement closing date — not your payment due date. Those two dates are usually weeks apart. So if your statement closes on the 15th and your payment is due on the 10th of the following month, the balance that gets reported is whatever was on your account around the 15th.2

In other words, even if you pay in full every month and never carry a balance, a high statement balance can still show up on your credit report and affect your utilization.

The Simple Fix

How to Find Your Statement Closing Date

- Open your last statement PDF or your card issuer’s app and look for Statement Closing Date or Statement End Date.

- Set a reminder 3–5 days before that date to give your payment time to post.

- If you are unsure, calling your card issuer to ask is a straightforward option.

Simple Example — Why This Works

| Scenario | Balance Reported | Limit | Utilization Reported |

|---|---|---|---|

| Pay on due date only | $450 | $500 | 90% |

| Pay $400 before statement closes | $50 | $500 | 10% |

Same spending. Same card. Same payment amount. The only difference is when the payment was made relative to the statement closing date.

5) Fast Ways to Lower Utilization (Ranked by Speed)

If your utilization is higher than you would like, here are the most common approaches, ordered roughly by how quickly they can affect your reported balance:

- Pay before statement close. This is the fastest way to change what gets reported in the next cycle.2

- Make two payments per month. One mid-cycle payment and one before the statement closes can prevent balances from climbing too high before reporting.2

- Spread spending across cards. Instead of putting everything on one card, distributing charges helps keep any single card from reporting high.

- Request a credit limit increase. If your spending stays the same but your limit goes up, your utilization percentage drops. This only makes sense if spending stays stable — increasing the limit and then spending more does not help. Also worth knowing: if an issuer lowers your limit without warning, your utilization can increase even if your balance has not changed. Checking your credit reports periodically helps catch this early.2

- Check for reporting errors. A wrong limit or an incorrectly reported balance can inflate your utilization. If something looks off on your credit report, it may be worth disputing.

FAQ

Does utilization reset every month?

Utilization can change from month to month because lenders report new balances regularly. This makes it one of the faster-moving credit factors. Paying down a balance before your statement closes can show improvement in your reported utilization within the next cycle.2

Should I focus on overall utilization or per-card utilization?

Think of it like a GPA: your overall utilization is your average across all cards, but a single card reporting very high is like one failing grade dragging down the average. Both numbers matter to scoring models. If time or funds are limited and only one thing can be addressed, one common approach is to prioritize any single card currently reporting above 50% — that tends to have the most visible impact on the overall picture.2

Does 0% utilization hurt my score?

Not exactly — but 0% and near-zero are not quite the same. According to Experian, having some activity reported across your cards is associated with slightly stronger results than reporting zero on every account. The consistently strongest range is between 1% and 9% utilization. Reporting very low utilization can be fine, but scoring results can vary by model. Some credit education sources note that very small reported balances may perform differently from every account reporting zero. The practical takeaway is simple: avoid high reported balances, especially on any single card.2

Does checking my utilization or credit report hurt my score?

No. Checking your own credit report or score is a soft inquiry and does not lower your score. Hard inquiries — which happen when you apply for new credit — are what can temporarily affect your score.2

Where can I check my credit reports for free?

In the U.S., the official source for free credit reports is AnnualCreditReport.com. The CFPB notes that free weekly reports through this site have been permanently extended. Checking all three bureau reports (Equifax, Experian, TransUnion) is worth doing since each can show slightly different information.3

Will paying my full balance always fix high utilization?

It depends on timing. If you pay in full after the statement closes, that full balance may already have been reported. Paying down the balance before the statement closes is what lowers the number that gets sent to the bureaus.2

What to Do Next

Start by finding the statement closing date on your most-used credit card. It is usually listed on your most recent statement PDF or inside your card issuer’s app under “Statements” or “Account Details.” That date — not the payment due date — is when your balance is typically reported to the bureaus.

If any card is currently reporting a high balance, paying it down before that closing date is the most direct way to lower your reported utilization in the next cycle. A payment made even a few days before the statement closes can result in a noticeably lower number being sent to the bureaus.2

From there, check each card individually — not just the combined total. One card sitting near its limit can pull your score down even when everything else looks fine. Once you know which card is the problem, that is the one to address first. Pulling your free credit reports at AnnualCreditReport.com shows you the reported balances and limits the scoring models are actually seeing.3

References

-

myFICO. “Amounts Owed” — utilization concept and keeping balances low.

Source -

Experian. “Is 0% Utilization Good for Credit Scores?” — targets under 10% and below 30%; reporting near statement close; paying before close; soft vs. hard inquiries.

Source -

CFPB. “How do I get a copy of my credit reports?” — free weekly access permanently extended; official instructions for AnnualCreditReport.com.

Source

Disclosure: This article is general education, not financial advice. Credit scoring, lender criteria, and reporting practices vary by bureau, lender, product, and time.